DOUBLE TRIGGER CONTRACTS

(May 2022)

Alternative Risk Transfer arrangements are typified by

modifications of previous, proven methods that enhance an organization’s

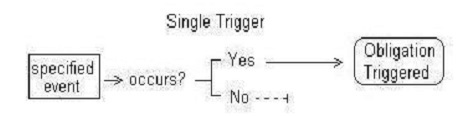

ability to deal with major risks. Under traditional insurance and reinsurance

contracts, the insurer’s obligation to pay for a loss is initiated by a single

event or trigger.

|

Example: Single

Trigger Event |

||

|

1. Insured and Insurer

agree to issue an insurance policy based on parameters for eligible source of

loss. |

2. Within the

applicable policy period, an eligible loss occurs. |

3. The insurer’s

obligation to investigate loss and make payment is triggered. |

Single Trigger contracts, obviously, continue to work very

well in most traditional coverage situations. The simple variation, of adding a

second trigger creates a vastly different circumstance.

|

Example: Double

Trigger Event |

||

|

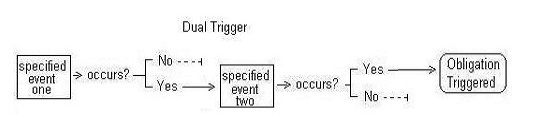

1. Insured

and Insurer agree to issue an insurance policy based on parameters for

eligible source of loss and upon two, independent events. |

2. Within the applicable policy period, an eligible loss

occurs. |

3. The insurer’s obligation to investigate loss and make

payment has not been triggered, so no action occurs. |

Obviously, a single, unaccompanied occurrence or event has

no effect on a double trigger contract.

However, an additional action does:

|

Example: Double

Trigger Event |

||||

|

1. Insured and Insurer

agree to issue an insurance policy based on parameters for eligible source of

loss and upon two, independent events. |

2. Within the

applicable policy period, an eligible loss occurs. |

3. The insurer’s

obligation to investigate loss and make payment is NOT triggered. |

4. A second event

occurs within the coverage period that meets the contract parameters. |

5. The insurer’s

obligation to investigate loss and make payment IS triggered. |

Similarity to

Reinsurance

In one respect, a traditional reinsurance contract (treaty)

is a rudimentary version of a double trigger contract. In order for a loss to

qualify for coverage:

1.

Eligible losses have to occur

2. The

volume of eligible losses has to reach an amount that breaches the primary

level of insurance

The resemblance to a typical double trigger agreement ends

there. Under a traditional reinsurance arrangement, the triggering situations

are not independent. Reinsurance merely depends upon a requisite volume of

eligible loss or losses. However, a double trigger contract adds a necessary

twist.

Double Trigger Twist

Unlike traditional reinsurance contracts which operate,

essentially, by relying on two related events (occurrence of eligible loss(es)

at a given level either via frequency or severity), a double trigger contract

relies on independent events. Since the two events usually have little or no

relationship with each other, they are particularly well-suited for use in

covering catastrophic loss exposure.

|

Example: A global corporation’s revenue is

generated by dozens of different business operations in different parts of

the world. However, the corporation knows that it is still vulnerable if it

suffers a major loss involving its manufacturing property holdings in several

coastal areas or to unanticipated increases in certain metal supply costs. It

arranges for catastrophic reinsurance for losses that exceed thirty million

dollars, but only if, in the same policy year, its particular supply cost

increases by more than 40%. In a given year, this company presumes that it is

healthy enough to absorb either a catastrophic-level property loss or a huge

increase in critical supply costs, but not both. |

As an ART measure, use of double trigger contracts can be

very complex. They are usually designed according to considerations of

financial and underwriting risk and the former is not an area that is,

traditionally, addressed by insurance. Double trigger agreements are often far

more difficult to price since little or no actuarial or other supporting data

exists.

Whether an insurer or a non-insurance entity provides

multi-trigger coverage, the triggers are uncorrelated. The lack of correlation

substantially reduces the probability that all of the qualifying events will

take place. The lower probability increases the insurability of a given

exposure and the cost is substantially less than what is available under

comparable, single trigger policies. Typically, multi-trigger arrangements involve

pairing an insurable event with some form of financial index rather than two or

more insurable events. Under the former arrangement, there's a chance that the

product will be treated as a financial derivative rather than an insurance

policy (even if the contract is provided by an insurer).

When dealing with high-stakes exposures, such agreements

need to revolve around two conditions that are not only independent, but they

also should be highly unlikely to occur even singly during a given period of

time. In other words, the conditions should be both independent and

extraordinary. Triggers that do not meet both of these requirements are

useless.

|

Example: Insurer

A desires a double trigger reinsurance agreement with Reinsurer A. Insurer

A’s current book of business is as follows: |

||

|

Line of Business |

Annual Premiums |

Where Written |

|

Commercial

Automobile |

$174,000,000 |

|

|

Commercial Property |

$106,000,000 |

Midwestern |

|

Misc. Professional Liability |

$ 22,000,000 |

Midwest and |

|

Equipment Breakdown |

$ 8,000,000 |

Continental |

|

Insurer A buys a reinsurance contract. The first trigger

requires it to be reimbursed for all vehicle liability losses that exceed

forty-five million dollars in a given calendar year. There is a second

trigger and the likelihood of some coverage being paid changes drastically,

depending upon the trigger: Scenario

1: The second trigger is losses exceeding twenty million in losses in

Commercial Property Scenario

2: The second trigger is losses exceeding twenty million in losses in

Miscellaneous Professional Liability Scenario

3: The second trigger is losses

exceeding twenty million in losses in Equipment Breakdown. |

||

In light of the lines of business and the areas in which the

business exists, each scenario presents a vastly different likelihood of being

reached.

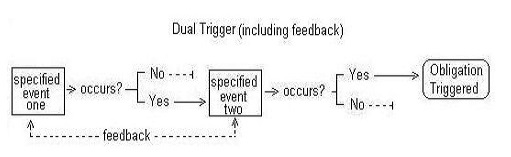

Trigger

It is very important to take the reference to independent

triggers with a level of skepticism. If you study any elements that are used as

triggers, you will discover that there IS some level of dependency. Triggers

represent types of losses that affect a given business; they also have a

certain probability in a given operating year. It is the potentially disastrous

occurrence of both (or more) of such elements that can threaten a company’s viability.

Generally, the situations that are used as triggers are a

result of carefully reviewing a company’s operations and its previous loss

history, particularly large losses. An effective double or multiple trigger

contract is NOT one that is impossible to occur, but rather one that a level of

likelihood that, while very low, still has a level of probability that will

trigger protection against rare catastrophes.

The fact that there is some level of dependency means that

pricing and underwriting the coverage are affected.

Note: This is a

very simplified discussion of the double trigger concept. In the worlds of

reinsurance and ART, this risk management method is being used in a wide

variety of ways. Its effectiveness is still in dispute due to the lack of

standard pricing, statistics and other measures involving its use.